Invest Europe: Key findings 2017

Invest Europe published its annual report on investment and fundraising for the European private equity and venture capital industry. The report covers activity on over 1,250 firms, directly verified by fund managers using the European Data Cooperative (EDC). The EDC holds data from over 3,000 European private equity firms on 8,000 funds, 64,000 portfolio companies and 250,000 transactions since 2007. The research is recognised by coverage in the Financial Times.

The investment market is booming

Findings in the report paint a delightful picture of the Investment development in Europe. Fundraising reached €91.9 billion, surpassing 2016 by 12% and the highest level since 2006. Pension funds provided 29% of all capital raised, followed by funds of funds (20%), family offices & private individuals (15%), sovereign wealth funds (9%) and insurance companies (8%).

Private equity hits ten-year high

Simultaneously Private equity investment in European companies hit a ten-year high at €71.7 billion, a 29% year-on-year increase. Almost 7,000 companies received investment, of which 87% were small and medium-sized enterprises (SMEs). Divestments (measured at cost) increased by 7% to €42.7 billion. This is the third highest level of the past decade, with around 3,800 European companies exited in 2017. Venture capital investment increased by 34% to a ten-year high of €6.4bn, surpassing 2008’s amount by 13%. Nearly 3,800 companies were venture-backed, an 8% increase.

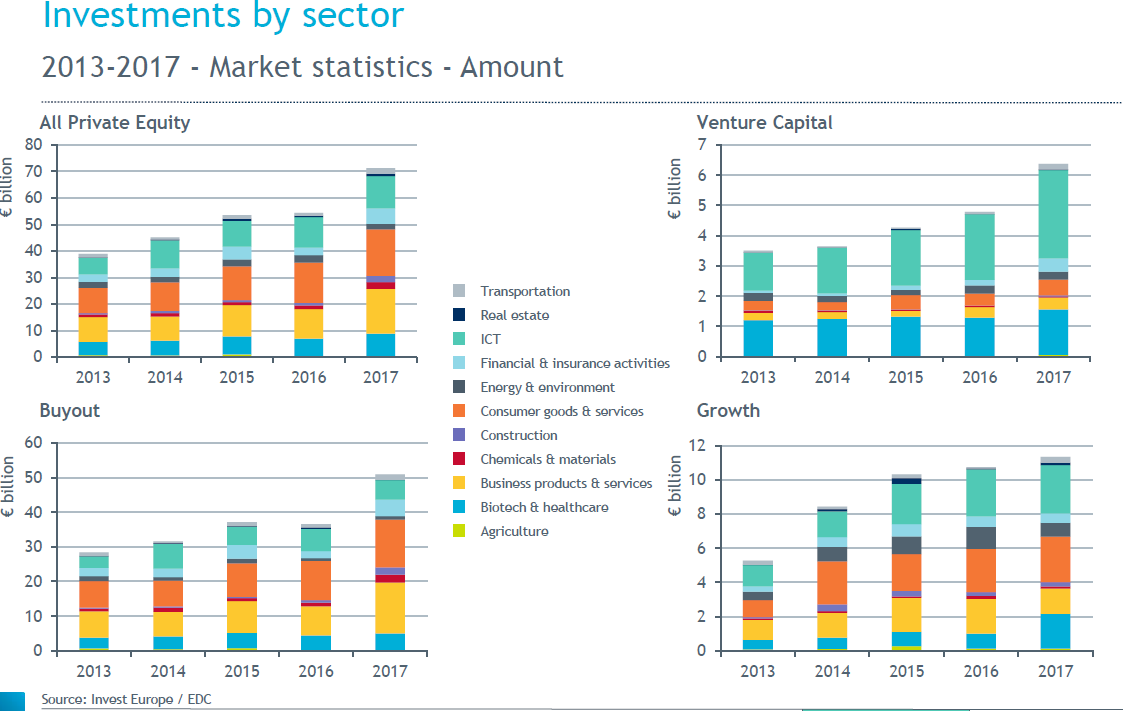

PE investments by industry

Companies focused on consumer goods and services in Europe received 15% more private equity investment compared to last year, representing 24% of the total. Almost equalling this were business-to-business products and services, increasing by 51% to account also for 24% of the total. The technology sector (ICT) reached a ten-year investment high, with 17% of the total, a year-on-year increase of 6%.

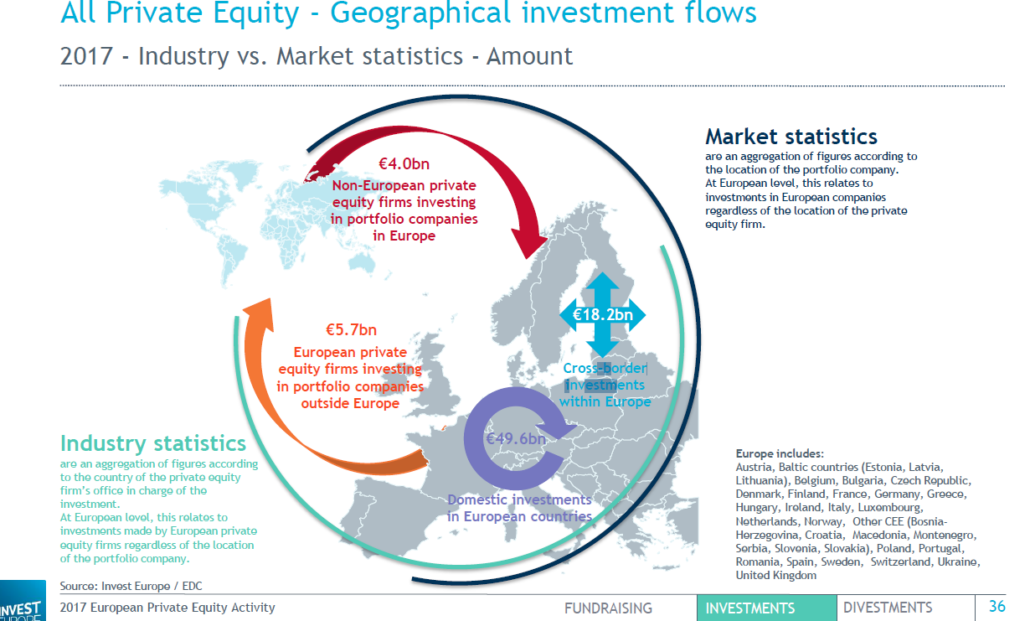

Geographical Distribution of the Investments

France and Benelux-based companies received 27% of private equity investments in 2017. Close behind was the UK & Ireland with 26%, followed by DACH-based companies (20%), Southern Europe (13%), the Nordics (9%) and CEE (5%).

{kind=link}

{kind=link}