Europe’s VC reset – recovery without a cycle reset

This article offers a focused insight into one of the core mechanisms shaping markets in 2026. The full Market Outlook 2026 provides the broader, integrated context across macro, public markets, private capital and digital assets.

Europe’s venture environment has moved into a recovery phase characterised by improving activity and clearer thematic focus – while remaining structurally selective rather than broadly risk-on.

This distinction matters. A rebound in funding and sentiment does not automatically translate into unconstrained growth. Outcomes remain tied to liquidity, exit capacity, and the ability to scale beyond early success.

Rebound numbers – activity returns, selectivity persists

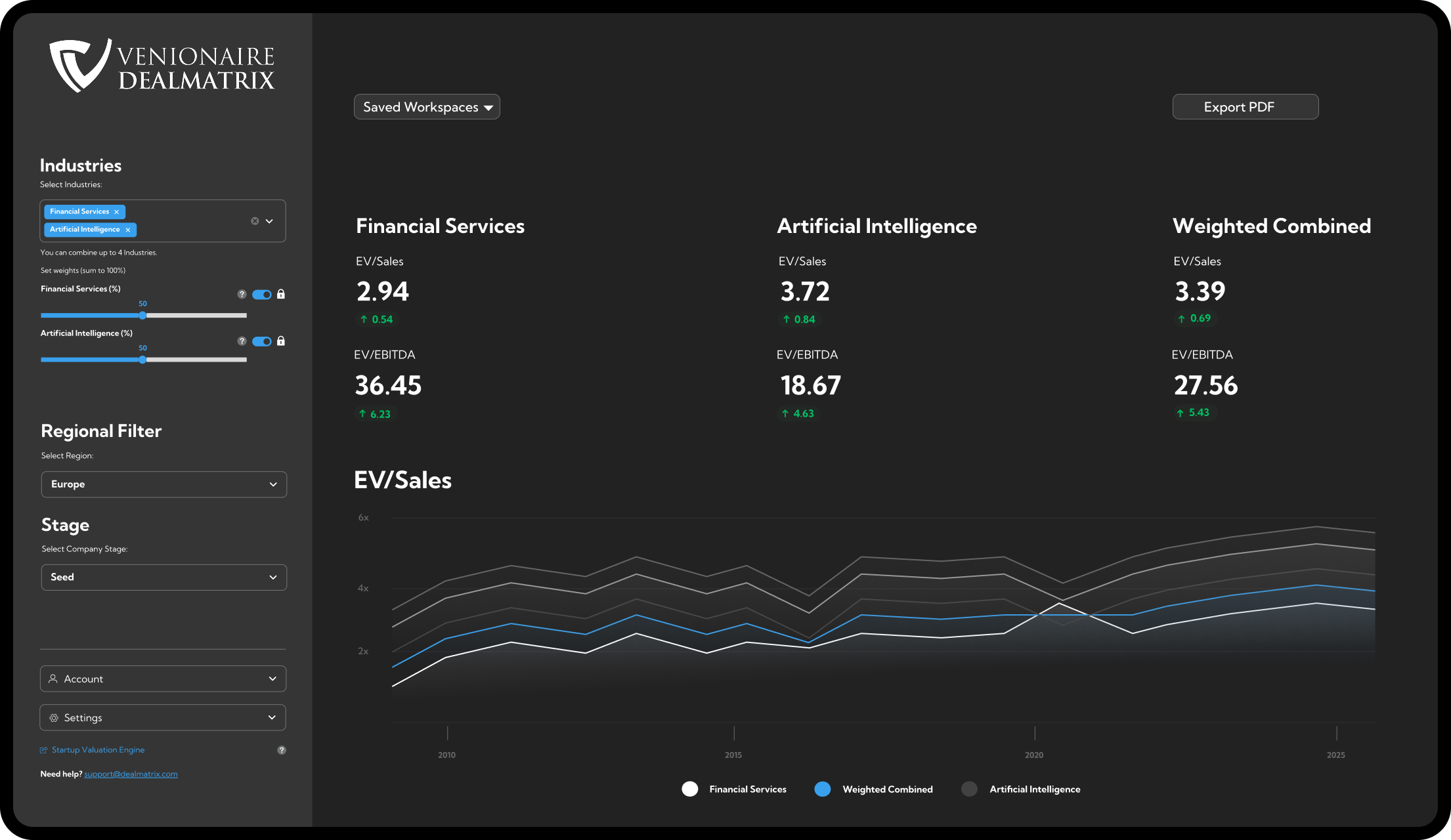

European venture activity recovered in 2025, reaching USD 65.9 bn across 3,784 transactions. Capital deployment, however, remained uneven across stages:

- Late-stage: USD 26.6 bn across 781 deals

- Early-stage: USD 18.8 bn across 662 deals

- Technology growth: USD 13.7 bn across 83 deals

- Seed and angel: USD 6.7 bn across 2,258 deals

Sentiment indicators stayed above neutral throughout the year, pointing to renewed confidence without a return to indiscriminate allocation.

Mechanism: Recovery is taking place inside a constrained capital regime – where liquidity and realisation pathways determine which companies can convert momentum into durable outcomes.

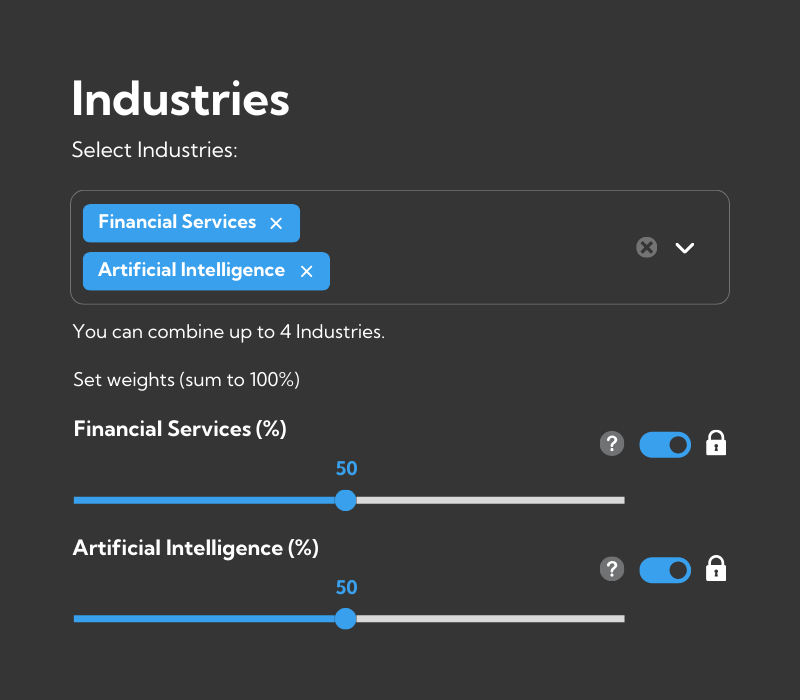

Thematic specialisation – depth as Europe’s advantage

Europe’s recovery is underpinned by thematic concentration rather than broad-based exposure. Capital continues to cluster around areas with established regional depth:

- Targeted AI specialisation, moving beyond general experimentation

- Applied AI and infrastructure layers such as compute, data tooling, chips, and AI safety

- ClimateTech and the wider energy transition

Into 2026, the shift is from horizontal technology narratives toward domain-specific applications and infrastructure that can justify selective capital deployment.

Mechanism: Specialisation supports recovery only when it creates defensible scaling paths – not when it simply accelerates early validation.

The scale gap – Europe’s unresolved champion problem

A persistent structural constraint remains Europe’s difficulty in building global champions.

Venture-backed companies frequently achieve technical and commercial validation but are absorbed before reaching full scale, resulting in the export of intellectual property and long-term value creation.

The emergence of new unicorns in 2025 signals renewed formation capacity, but does not resolve the scaling bottleneck on its own. Without sufficient late-stage capital and liquidity mechanisms, exits risk becoming the default outcome rather than a strategic choice.

Late-stage growth capital and secondaries are therefore positioned as structurally important tools for extending holding periods and supporting scale.

Mechanism: Recovery strengthens the pipeline – but without deeper scaling infrastructure, it reinforces the same pattern it seeks to overcome.

What to watch in 2026

The binding variable is not sentiment, but realisation.

Key questions:

- Do exit channels broaden beyond episodic windows?

- Do secondaries normalise as a structural liquidity instrument?

- Do barriers to scale meaningfully decline, enabling value to compound locally rather than being exported?

Why this matters

Europe’s VC reset is not a cyclical replay. It combines recovery with selectivity – while leaving the central challenge unresolved: scaling champions instead of exporting IP.

The broader framework that connects venture dynamics to liquidity, exits, and the cross-asset environment sits beyond this mechanism view.