Finding Disruptive Innovation

Two years ago one of our Private Bankers introduced me to Dr. Günther Dobrauz, a Director of PWC (CH) and former Venture Capital Fund Manager, at a meeting in Zürich, Switzerland. This meeting turned out to be one of the most interesting ones I have had for quite a while. He explained to us a model (Technology BridgeTM)) he had developed and recently published in his book “Uptake Revisited – An Investigation into the Success & Failure Factors for Innovative Products in International Markets”.

We are always looking for innovative approaches to make better investment decisions and to improve our own models, which we use in our consulting activities. We examine new models quickly and test them internally for a while – as we need to convince ourselves of a significant impact on our field. When it comes to high-technology driven private equity transactions, we need to rely on facts instead of magic crystal balls.

This might sound funny, but there is a substantial number of private investors and venture capital firms out there who will not bother running a professional deal selection process. Simplified, this would usually consist of the following steps:

1. Does it fit our investment focus?

2. How does it score on standardized screening criteria?

3. Are there any “Red Flags” from a financial, technological or legal due diligence?

No kidding, quite a large number of investors will make an investment decision on a so called “gut feeling”, “goodwill” or “rule of thumb” method. We have observed this biased habit. Fair enough – there are some successful business angels who prove that this is not the worst idea, ever. In professional terms, however, this method is not predictable; rather, it is quite fuzzy, as these “success factor heuristics” can be very different and probabilities of success and failure are very unclear. It is like it is in gambling, once in while there are winners, but the odds are not in favor of the player.

This method concentrates on the quality of the team. There is a significant number of very successful founders, who have changed their entire business – sometimes through an accelerator program (e.g. Y Combinator or Techstars) or with a first mentor (Business Angel) on board. In a very early stage of a startup, I agree that it makes sense to concentrate on the quality of a team, much more than later in a venture capital round. In early stages products and technologies may change a couple of times.

Venture capital funds on the other hand need to be clear and transparent when it comes to their deal selection criteria. Investors of the funds (so called “Limited Partners”) will require a full understanding of the competitive advantages of a specific fund. They will be interested in how you will gather the best deal flow, –screen and select deals, perform best in business development and most importantly how you plan to exit your portfolio. All of this is required prior to an investment into a venture fund, where investors will commit money for 8 to 10 years, with the intention to get it back with a nice return on top. Therefore funds will follow their rule sets quite strictly.

Dr. Dobrauz developed a smart, comprehensive approach to investigate the disruptive innovation potential of technology driven projects and companies with a true practical intention, namely for a venture capital fund he worked for at the time. His approach has a strong theoretical basis and is very simple to use. He explains in his statement of hypothesis: “The market cycle can be modeled as the development of five interlinked S-curves of “achievement over time” […]”.

These five interlinked S-Curves are:

– “sales of existing products”,

– “valuation of new product”,

– “technical development of new product”,

– “customer satisfaction of new product” and

– “sales of new product”.

He explains further that successful innovation most probably takes place in three windows of opportunity:

A – “Technology BridgeTM“ – “Innovation steps up!”

The existing product is selling well with 85-90% market penetration, but a replacement technology is in development. Although only 15-20% complete, the valuation of this product is already over 50% of its final value.

B – “Crossing the Chasm” – “Change in mass markets”

The new product is being sold to > 10% of the market (pre-chasm), even though only at 75% of technical “perfection”.

C – “Renaissance” – “The company needs something new to maintain value”

The new product has 50% of its eventual market penetration, technical development is complete and the valuation can top out. Soon the cycle will start over again.

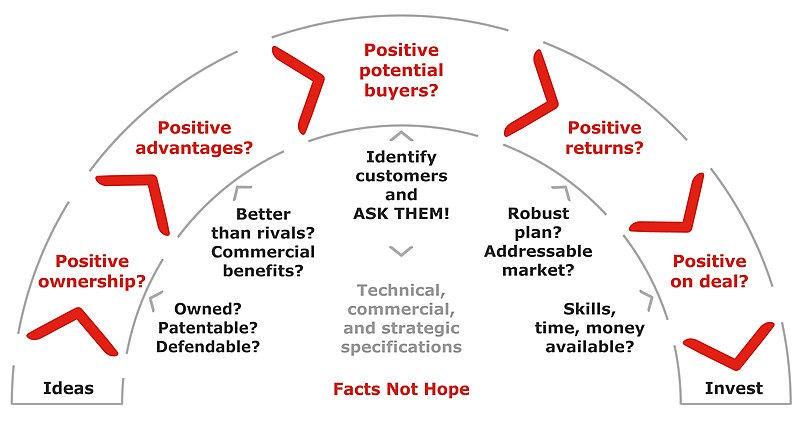

The results show that market uptake can be predicted quite well using a simple set of five option selection principles (questions), which are the same for all three windows. This approach was tested with data of 291 companies, out of which 6 had positive answers to all questions. The five questions analyze technical, commercial and strategic specifications.

Source: https://commons.wikimedia.org/wiki/File:Technology_Bridge_by_Guenther_Dobrauz_Saldapenna.jpg

1. Positive ownership?

2. Positive advantage (to the costumer)?

Note: Deal screening needs to be performed very efficiently. As 80% of the opportunities have been filtered out after the first two questions (50% of the reviewed opportunities in this study were not found to be cleanly and legally owned by their proponents and a further 30% offered no advantage above already existing products and services) it is recommend by the author to use them first.

3. Positive potential buyers?

4. Positive returns (possible)?

5. Positive on deal?

In practice we have found the last question to be among the most important. A positive investment decision has to fit the availability of skills, time and money of the investor at a given time. Even the best deal in your pipeline will not have a full chance to perform at its potential if you – as the investor – lack resources. Startups and investors should think about this point very carefully!

We like this approach, even though we found some critics concerning the missing factor “team” discussing it. Team quality or qualification is not analyzed at all. If you would process this model stand-alone, you would most likely miss to investigate one of the most important potential success- or failure factors of an early stage startup. Venionaire Capital provides popular services for technical valuation and due-diligence support. Our clients (startups or investors) profit from our unbiased insights, high quality research our proprietary mix of valuation and analytic models. Over the past few years we have developed a number of extensions for standard models and some internal models for technology- and company valuation. We work closely together with a number of universities and leading academic professors. Contact us to find out more.